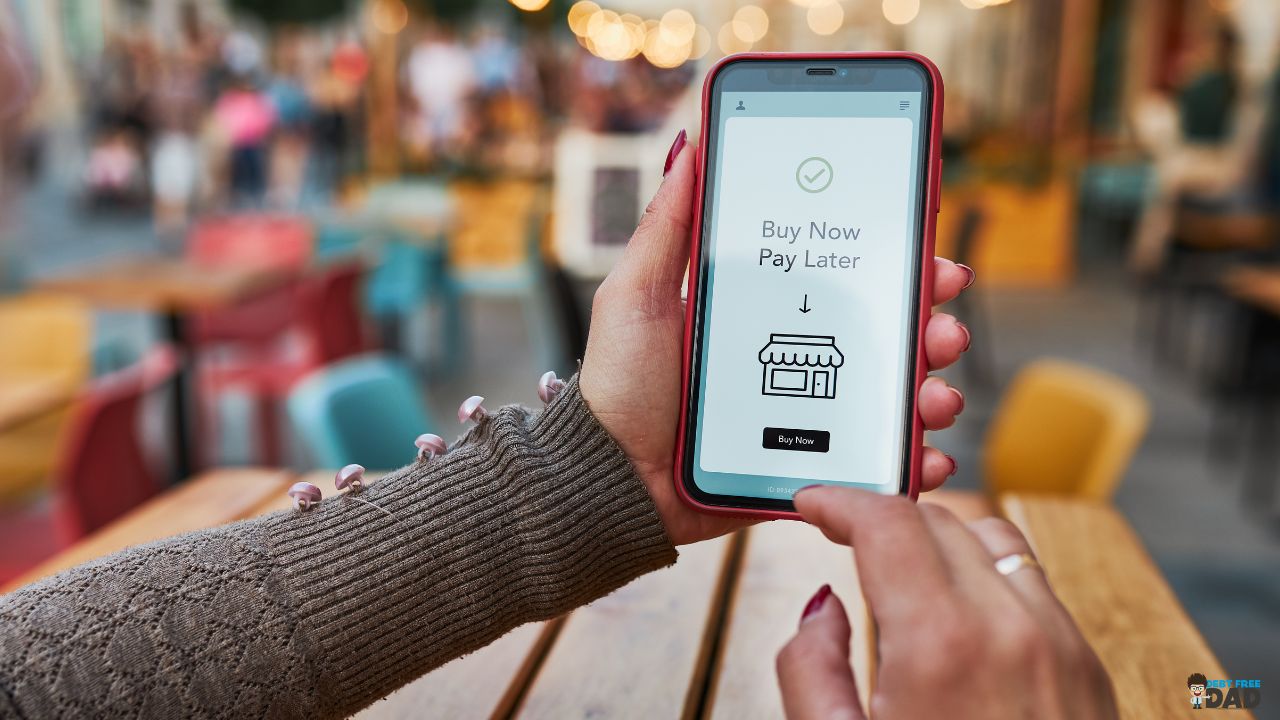

Is this you? Staring at you online cart, wanting something we know we probably shouldn't buy. And then, like a magic wand, the "Buy Now, Pay Later" option appears. It feels like a guilt-free way to get what we want without feeling the immediate pinch in our wallets.

But as folks who have battled our way out of debt, we know that anything that sounds too good to be true usually is. These BNPL services are designed to make you spend more. In fact, some studies show that people spend significantly more when they use BNPL compared to other payment methods.

That small, seemingly harmless "pay in 4" option at checkout can actually be a slippery slope into a mountain of debt?

You're about to buy something online, and a little box pops up, offering to split your purchase into easy, interest-free payments. It's called "Buy Now, Pay Later" (BNPL), and it's everywhere. It feels like a smart way to manage your money, right? But for many of us who've crawled our way out of debt, we know that easy payment plans can sometimes be a wolf in sheep's clothing. This week, we're going to break down what BNPL is, how you can use it to your advantage, and when you should run in the other direction.

Buy Now, Pay Later is essentially a short-term loan.

Companies like Klarna, Afterpay, and Affirm partner with retailers to let you get your items immediately while you pay for them over a set period, often in four installments. The big appeal is that if you pay on time, there's usually no interest.

Think of it this way: you need a new set of tires for your car, and it's a purchase you can't put off. The total is $600. Instead of putting it on a high-interest credit card, you could use a BNPL service to break it down into four payments of $150 every two weeks. If you know you have the money coming in to cover each payment, it can be a helpful tool to manage your cash flow without derailing your budget

Why People Fail with BNPL

The biggest trap with BNPL is how easy it makes spending money you don't have. That instant gratification of getting something now can be incredibly tempting. It's easy to lose track of multiple BNPL plans, and before you know it, you have several small payments coming out of your account, which can add up to a big problem. Many people also fall for the "it's only $25" mindset, forgetting the total cost of the item.

The danger lies in what financial experts call "loan stacking." You might have a $50 payment for that new pair of shoes, a $30 payment for a concert ticket, and a $75 payment for a new gadget, all from different BNPL providers. Individually, they seem manageable. But together, they create a constant drain on your bank account, making it harder to cover your essential expenses.

And what happens if you miss a payment? Those "interest-free" promises often disappear, and you can be hit with late fees and, in some cases, high interest rates that are retroactive to the purchase date. Suddenly, that "deal" becomes a very expensive lesson.

The key to not falling into the BNPL trap is to treat it like any other debt. Before you click that "pay later" button, ask yourself: "Can I truly afford this right now?" If the answer is no, BNPL isn't the solution. Always keep a list of your ongoing BNPL plans and their due dates. Set reminders for payments to avoid late fees, which can be hefty and are how these companies make a lot of their money.

Don't let the convenience of today steal from your financial peace of tomorrow. Take control of your spending by being honest about what you can afford, and use BNPL as a planned tool, not an impulse buy.

So, how can you use these services without getting burned?

It comes down to a simple rule we've learned the hard way: only use BNPL for things you absolutely need and that you've already budgeted for.

Let's really break that down because it’s the most important defense you have against the BNPL trap. Think of it this way: your budget is your plan for the money you actually have. BNPL shouldn't be a magic wand to create more money; it should be a tool to manage the timing of your spending when life throws you a curveball.

We like to call this using it as a "cash flow management tool." It's not for "affording" things you can't actually buy with your own money. Instead, it’s for bridging a short-term gap between when you need something essential and when your next paycheck lands.

Maybe your only pair of work shoes just fell apart, and you need a new pair to do your job. Or your kid has a school trip next week that requires a specific piece of equipment you just found out about. These are necessities. Using BNPL here, when you know the money is coming, can be a lifesaver.

Now, let's contrast that with the "want" scenario. You're scrolling online and see a flash sale for a designer handbag or the latest noise-canceling headphones. They're 50% off, but still $300. You don't have a spare $300 in your budget this month. That little voice in your head might say, "But with BNPL, it's only four payments of $75! I can swing that!"

This is the danger zone. You're not using it to manage cash flow for a necessity; you're using it to stretch your budget for something you desire but can't truly afford. What happens is you're now committing future you to payments for a past want. When an actual emergency pops up next month – a flat tire, a sick pet – that $75 is already spoken for, making a stressful situation even worse. The excitement of the purchase is replaced by the long-term anxiety of debt.

Fifty-eight percent of BNPL users turn to the service to purchase something they couldn't afford with traditional payment methods, according to data from the Federal Reserve.

This is where you have to be brutally honest with yourself, and it's a muscle we all had to build on our own debt-free journeys. Is this item worth sacrificing your peace of mind? Is that temporary buzz from a new purchase worth the nagging stress of another bill to pay? As people who have climbed out of debt we can tell you with 100% certainty that it's not. The incredible feeling of being in control of your money, of knowing you have a buffer for the unexpected, is far more valuable and rewarding than any impulse buy. That control and peace of mind is what true financial freedom feels like.

Responses